Escrow is a term you will hear a lot in real estate. It refers to a key part of negotiating and concluding a real estate transaction.

It is also used after the sale in a different way to make sure essential property ownership expenses are paid properly.

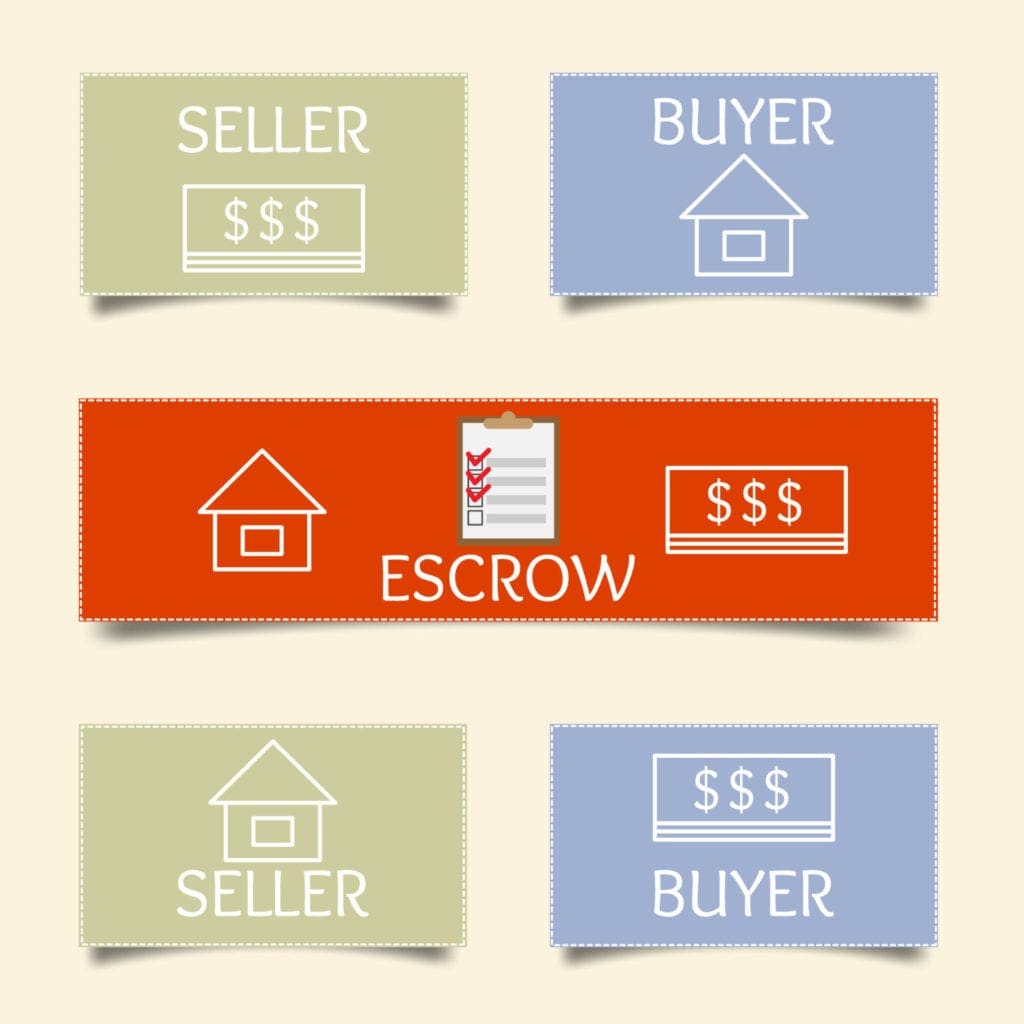

What Is Escrow?

Although it may be unfamiliar to you, escrow is a concept that has been around for a long time. Basically, escrow gives buyers and sellers a way to hand something valuable, like money or a deed, to a third party.

The third party is supposed to be neutral and trustworthy. Their job is to hang onto the money or document until all conditions of the deal are met. Only then will the seller get the money and the buyer get the deed.

Escrow is a legal concept, and an escrow agreement is a legal document. This agreement describes the terms and conditions that have to be met before items in escrow are released.

When buying and selling real estate, a person called an escrow agent oversees the escrow arrangement. This is often a representative of the title company. Sometimes it is a real estate attorney.

Uses for Escrow

Escrow is part of most real estate deals. Whether it’s an individual buying a single-family home or an investor group purchasing a chain of hotels, escrow is a key element.

Home Purchases

Nik Symkin/Shutterstock

The main way escrow gets used is when a buyer makes an offer on a property. In order to show serious intent, the buyer usually puts up an earnest money deposit.

Earnest money on a single-family home purchase ranges from a hundred dollars to several thousand dollars.

About 1 percent of the sale price is a common amount. A buyer may offer more earnest money to convince a seller that the buyer is serious.

Not all offers include earnest money. However, most sales contracts do, and it can cost a significant amount of money. That’s where escrow comes in.

If you are the buyer, you don’t write a check for earnest money and hand it to the buyer. Instead, the check will be held by the title company, acting as an escrow agent.

The escrow agent opens an escrow account. The earnest money check is placed in this account. At this point, the property is described as “being in escrow.”

As Collateral

Ordinarily, the sales offer document will describe how long the property will be in escrow. By the end of the escrow period, either the deal gets terminated or it moves toward closing.

The escrow period may be a few days or a few weeks. During this time, the property is inspected.

Unless it’s an all-cash deal, the seller will arrange for financing. Other details, like dates of possession and transfers of appliances, may also get hammered out.

If a serious glitch arises, the property may “fall out of escrow.” If you hear this term, it means the deal can’t be completed as is. Some reasons for falling out of escrow could include:

- The buyer was unable to qualify for a loan

- The property did not appraise high enough

- Some serious problem showed up during the inspection

Ordinarily, if the deal closes, the earnest money will be credited toward the purchase amount. If the buyer backs out during the option period, the buyer usually gets the earnest money back.

Establishes Intent

If the buyer doesn’t act before the option period ends, the seller may get to keep the earnest money. The escrow agent has the job of seeing that earnest money goes to the right party if the deal folds.

The escrow agreement describes how and when this works. Escrow is set up to protect both buyers and sellers. Buyers don’t risk sellers taking off with deposits and selling houses to someone else.

Sellers know buyers have put up evidence of good faith, with a legal document protecting sellers’ interests. The escrow officer who plays a role in all this expects to get paid for the trouble.

The escrow fee, as it’s called, will usually be from 1 percent to 2 percent of the sale price. This fee is frequently non-negotiable and set by the title company.

Escrow After the Sale

Comzeal Images/Shutterstock

The other main use of escrow is after the closing. For this purpose, an escrow account is set up to collect the new owner’s payments for property taxes and insurance.

The account also pays the taxes and premiums in full and on time. The loan company opens this escrow account. Part of the monthly mortgage payment consists of a portion of the insurance premium and property tax owed.

Usually, this is one-twelfth of the annual amount for both bills. When insurance premiums and property taxes are due, the escrow account pays the insurance company and taxing authority. This is a convenience for homeowners.

They don’t have to save up and write big checks for insurance and taxes every year. It also protects the mortgage company by making sure insurance and taxes are paid.

Tip: Some deals don’t have this sort of escrow account. The new owner may prefer to write the checks themselves. This lets them hang onto and perhaps earn interest on money that would otherwise pile up in the escrow account.

RESPA Rules

The Real Estate Settlement Procedures Act of 1974 (RESPA) is a federal law that establishes guidelines for funding and managing escrow accounts.

One of this law’s main elements is that it limits how much a lender can make a borrower keep in an escrow account.

RESPA says lenders can have a cushion to cover increases due to higher taxes or insurance rates. It limits this excess to one-sixth of the total annual amount paid from the escrow account.

The federal law doesn’t require lenders to pay interest on money in escrow accounts. However, some state laws do.

Should You Use Escrow?

Escrow is not free and is not always easy to follow or convenient for everyone involved. However, its purpose and effect are to manage and reduce risk for everyone.

Escrow helps to see that everybody in the deal has their interests protected every step of the way. If you are buying or selling a home, you should insist on using escrow.