Recoverable depreciation is an important feature of many home insurance policies. Understanding and using it correctly can significantly increase the size of the benefit you, as a policyholder, receive on a claim.

Recoverable depreciation often makes it worth filing an insurance claim that would not otherwise exceed the deductible. However, there are some limits and special requirements to meet to receive the extra benefit.

Not all homeowner’s insurance policies include recoverable depreciation. And you may have to take specific actions in order to receive it.

Here are the basics about recoverable depreciation, including what it is and how to make the most of it.

Recoverable depreciation is worth understanding if you have a home insurance policy, so be sure to read this article until the end.

What Is Recoverable Depreciation?

To start, you need to understand the concept of depreciation. This is an accounting term that describes how to allocate the cost of an asset over its useful lifetime.

As time goes by, an asset experiences both wear and tear and obsolescence. This causes it to lose some of its value.

This is true of modern appliances such as refrigerators and television sets that may be covered by homeowners’ hazard insurance policies.

It’s also true of the house itself. All else equal, a new house is more valuable than an old house. This can be of particular importance when it comes to major parts of a house.

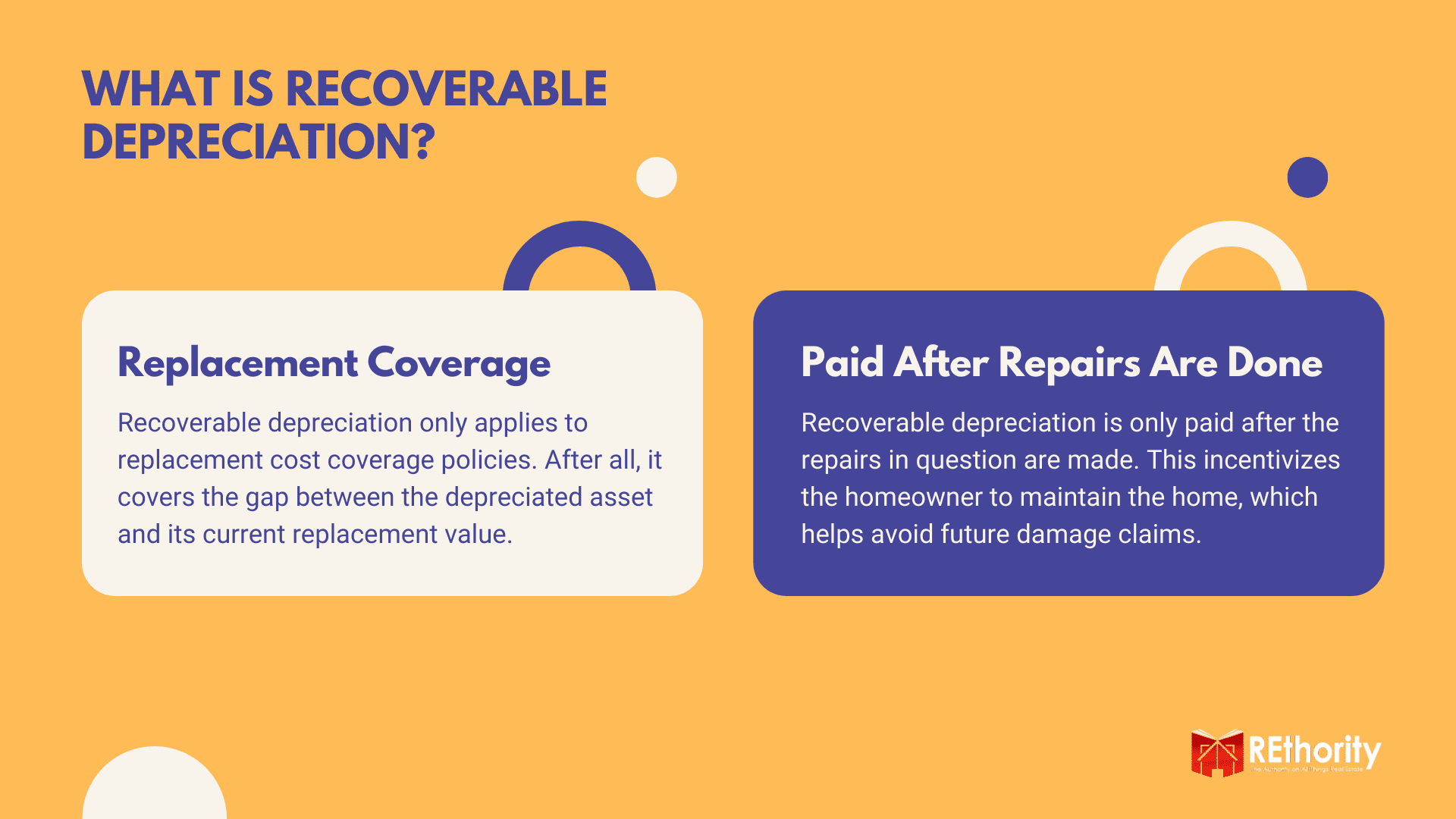

The roof is a part of the house where recoverable depreciation can make a big difference on a property insurance claim. With that in mind, here is our definition:

Recoverable depreciation is the difference between what property is worth after depreciation and what it would cost to replace it today.

It only applies to insurance policies with replacement cost coverage. In practice, after you make a claim, your insurance company gives you an initial payment for the actual cash value (ACV) of the property. This is equal to the depreciated amount.

After you repair or replace the damaged property, you’ll get a second check. This is the recoverable depreciation amount.

The total adds up to approximately the original cost of the property. Keep in mind, however, that if your policy has a deductible, you’ll have to pay that first.

How Recoverable Depreciation Works

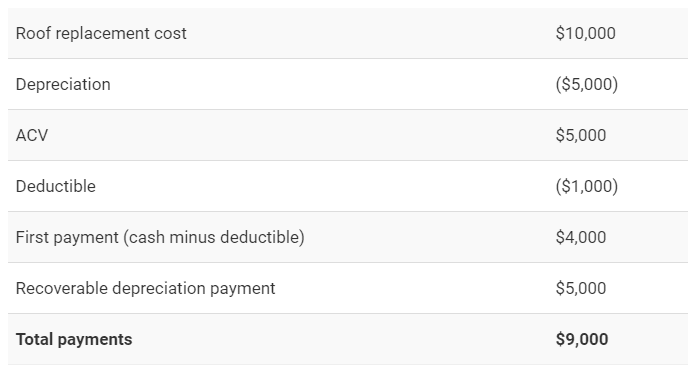

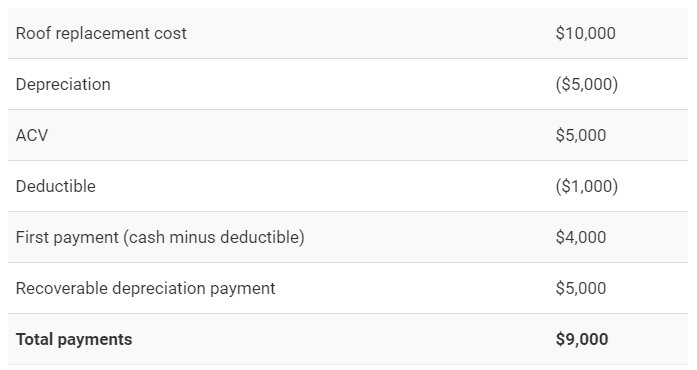

Let’s look at an example of how recoverable depreciation applies to an insured roof. The roof in this example cost $10,000 new. It was 10 years old when it was damaged by a hailstorm.

- First, you subtract the depreciation. To do this, start with the cost of the roof and its expected lifespan. In this case, we’ll say the roof’s expected lifespan is 20 years.

- After 10 years, the roof has gone through 50 percent of its expected lifespan. Multiplying $10,000 by 50 percent gives you $5,000, which is the depreciation.

- Next, subtract the depreciation from the roof’s cost. Taking $5,000 from $10,000 gives you $5,000. This is the ACV.

- Then, you’d subtract the deductible from the ACV. In this case, we’ll say the deductible is $1,000. Subtracting $1,000 from $5,000 gives you $4,000.

- When you file your claim for the hail damage, you’ll first receive a check for the ACV less the deductible. That comes to $4,000.

- Then, after you’ve replaced the damaged roof, you’ll get a second check for the recoverable depreciation. This check will be for $5,000, so your total claim will be $9,000.

Here’s a table explaining how it works.

As you can see, recoverable depreciation makes a big difference on this claim. There are some potential catches, however.

Using Recoverable Depreciation Correctly

M2020/Shutterstock

To get that second check from your insurance company, you have to actually repair or replace the roof or other property. This means you’ll have to use some of your own money, plus the first payment, to do the work.

Insurance companies do not like to pay more than it actually costs to replace or repair covered property on a replacement cost policy. This means there’s no benefit to you, the policyholder, in getting the work done for less than the full replacement cost.

You will likely have to show the insurance company the receipts for the work on the new roof. If the replacement costs less than the value of the roof, including recoverable depreciation, the insurance company will keep the difference.

Getting the roof damage repaired and paying for part of it out of your own pocket is not the only requirement. You may also have to complete the work by a certain deadline in order to recover the depreciated amount.

Recoverable Depreciation (Step by Step)

If you have made a claim on an item covered by recoverable depreciation, here are the steps to take to ensure your insurance policy pays up.

- Make your initial claim.

- After you receive the first check for ACV, get an estimate to repair or replace the damaged property.

- Get the work done and save any receipts, invoices, contracts, or canceled checks relating to the repair or replacement.

- Make copies of these for your files.

- Send either the originals or copies to the insurance company’s claims office.

It’s a good idea to include your claim number in any correspondence with the claims department. This includes when you submit the proof of replacement. The insurance company should be in touch to discuss any additional requirements.

Otherwise, you should receive a second check covering the recoverable depreciation. Different insurance companies have different claims processes. To be sure you are doing it correctly, check with your agent or claims representative.

Recoverable Depreciation Limits

Spok83/Shutterstock

Most, but not all, home insurance policies provide for recoverable depreciation. The difference between a policy with recoverable depreciation and an actual cash value policy can be sizable.

In the case of the roof claim above, such a policy would pay only ACV minus depreciation. That means receiving only a single $4,000 check instead of two checks totaling $9,000.

Must Replace Damaged Items

The key word in an insurance policy is “replacement.” If your policy covers replacement value, it probably means you will be paid for recoverable depreciation when you file a claim. If you are not sure your policy provides for recoverable depreciation, ask your agent.

However, not all property may be covered by recoverable depreciation. For instance, you may not be able to file a claim to recover depreciation on carpet damaged by a water leak.

Some Items Not Covered

Depreciation on an awning damaged by high winds may be non-recoverable depreciation. For this kind of property, you may be limited to ACV.

Also, keep in mind that if you spend more on the replacement than the original insured property, you will probably have to pay the difference yourself. The same is true if you can’t get the repair or replacement done for the cost specified by your policy.

Finally, if you decide not to get the roof replaced, the insurance will probably not pay for recoverable depreciation. However, you should still receive the first payment for ACV.

Recoverable Depreciation Roundup

Danielfela/Shutterstock

A policy providing for recoverable depreciation can be considerably more valuable (in terms of claim payments) than an ACV policy.

Recoverable depreciation allows you to replace valuable property with insurance proceeds instead of out of your own pocket.