When buying a home, most people simply go to the bank to finance their purchase.

At least, that’s the traditional way to do it, but it’s not the only one. Seller carryback loans, also known as seller financing, are another way to secure a home loan.

What Is Seller Carryback Financing?

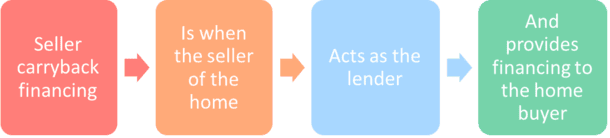

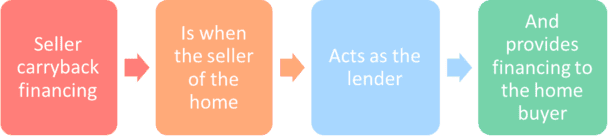

Seller carryback financing is an agreement between a seller and a buyer. The seller extends credit to the buyer instead of a bank or other financial institution. The buyer signs a promissory note with the seller.

A down payment is made, and installments are paid toward the purchase price over time. To put it simply, seller carryback is a way to finance a home purchase.

The seller receives the sale proceeds over time instead of in one lump sum. The seller “carries back” the price using a contract.

How Seller Carryback Works

Traditionally, real estate deals are backed by financial institutions. The bank provides the money for the purchase, while the seller supplies the deed of the home. The buyer puts money down (known as a down payment) and signs a promissory note to pay the remaining balance over time.

The title insurance company confirms the property has a good title. In seller carryback transactions, things work a bit differently. During this process, the seller still brings the property to the table.

Image Source: Thetruthaboutmortgage.com

The buyer pays a down payment and signs a promissory note. The difference is that the payment goes directly to the seller, not the bank. The title company still ensures the property has a good title, and the buyer carries insurance.

The middleman (the bank) is removed from this transaction. There is technically no loan granted. After all, the seller doesn’t provide the buyer with the money upfront, as a bank would. In its place, the seller has basically extended credit to the buyer for the purchase price of the home.

This will be repaid over time. Parties agree to financing terms before anything is signed or exchanged. The seller carries the balance, hence the name.

Seller Carryback Terms

D.Georgiev/Shutterstock

Terms for seller carryback financing are different from transaction to transaction. But a typical transaction includes:

Price

The first consideration is price. Without agreeing to a price, you won’t be able to set any other terms. You should never pay more than a property is worth.

However, you may find yourself buying a property at a premium when you negotiate a deal for a seller carryback.

This is because the seller is assuming more default risk. Buyers typically have lower credit scores, so sellers can get by with charging more for the property.

Down Payment

Sellers almost always want some sort of down payment before closing. This proves that the buyer has skin in the game.

Sellers may accept a smaller down payment than what is required using a conventional loan, but that’s really up to the seller.

When negotiating with a seller, don’t be afraid to ask for as little as a 3 percent down payment. But don’t be surprised if you’re asked to pay up to 10 percent.

Interest Rate

With long-term financing like this, you can pay more in interest than the original purchase price, so keep that in mind! It’s in the buyer’s best interest to negotiate as low an interest rate as they can.

Start Date and Payment Amount

Payments include both interest and principal. These are factored using a process called amortization.

Usually, amortization ranges from 15 to 30 years. Regardless of amortization terms, the deal needs to work for both buyer and seller.

Maturity Date

A maturity date is a date on which the entire principal balance must be repaid. This is normally when the amortization runs out. However, some lenders choose to use a balloon payment.

This is when a lump sum must be paid by a certain date. Seller carryback transactions typically include some form of balloon payment. This is important because it often means that the entire remaining balance is due.

For example, if your payments are $1,000 per month and your outstanding balance is $50,000, you’ll need to bring $50,000 to the table if the loan were to balloon today.

What typically happens is that you’ll have improved your credit score, so you can refinance the loan.

Instead of coming up with $50,000, a bank will loan you this money (remember, you’ve improved your credit score). Then, you’ll roll the loan into a traditionally financed mortgage.

Collateral

Most home loans are secured by the property itself. This ensures the lender has recourse in the event of default. However, there are times when a debt will be unsecured.

Credit cards are probably the most familiar form of unsecured debt that comes to mind because you don’t put up collateral for it. Real estate financing, on the other hand, is secured.

The deed of trust is pledged as collateral when you take out a mortgage. If payments aren’t made, the lender can foreclose. In seller carryback transactions, the home is the collateral for the promissory note. If the buyer doesn’t pay, then the deal is off and the seller keeps the house.

When to Use Seller Carryback Financing

Jinning Li/Shutterstock

Seller carryback financing is a great option for people who may not be able to qualify for a more traditional mortgage. Also, it’s a great way for investors who own multiple properties to reduce their credit utilization ratio.

Remember, they don’t have to take out multiple loans from a bank—the seller carries them! There are two different perspectives to consider when weighing the pros and cons of seller carryback financing: the seller and the buyer.

It’s important to look at the advantages and disadvantages of each. We like to look at each individually because they come with different considerations for each party.

Pros for the Seller

For the seller, this process can have many advantages. These include:

Income

A property being sold as a rental still generates income. This means the seller doesn’t have to give up the regular income. When they finance the sale, the income stream continues as ownership of the house slowly transfers to another party.

It’s Comfortable

If you’re going to take a gamble on backing the sale of a property, then it makes sense that it’s a property you’ve owned and cared for. You know what you’re getting into, and it’s a comfortable way to stretch your financial legs a bit.

Save on Taxes

When using seller carryback financing, the IRS allows you to defer capital gains on the sale of the property. This reduces your taxable income, also reducing your tax bill to Uncle Sam.

Good Return on Investment

In comparison to bonds and annuities, the interest you receive from the promissory note in a seller carryback transaction is usually better.

Plus, you can earn interest on principle, which isn’t something that would happen if the property were sold using a cash transaction.

Better Sales Price

When you compare a seller carryback arrangement with more traditional ways to mortgage a home, the seller is normally going to come out on top with their sales price.

You Put Up Collateral

While it may seem strange to see this in the positive category, when the property is the collateral in the deal, then any default on the promissory note means it just goes right back to you. So, you’re not taking a ton of risk.

Cons for Sellers

Of course, there are a few downsides sellers must be aware of when it comes to seller carrybacks. These include:

Lots of Negotiation

Literally every aspect of the transaction is negotiable with a seller carryback. Many people who sell their properties this way aren’t familiar enough with the process to be good advocates for themselves. If this describes you, it’s a good idea to seek advice from professionals.

It Takes Trust

A bank or other financial institution qualifies borrowers, and you need to do this as well. You must ensure that you can trust the buyer to take care of the property and make the payments.

In my years of managing investment properties, I’ve found that buyers typically skimp on maintenance. For this reason, I’d never enter into one of these agreements. However, this risk can be hedged by routinely inspecting the property.

Tax Liability

You’ll have to consult with an accountant or other tax professional to find out what the tax liability is on the property so that you can make sure you have enough money to pay the taxes associated with the property.

Inflation

A sale that is financed with a promissory note via a seller carryback transaction that has a fixed payment can be less valuable over time due to inflation. This may not be an issue for some sellers with sufficient assets, but it’s something to be aware of.

Pros for the Buyer

There are quite a few pros for the buyer when it comes to financing a home purchase with a seller carryback. These include:

Less Hassle

When you compare a seller carryback with a traditional mortgage, there is usually far less paperwork involved, which means less hassle.

It’s Negotiable

Trying to negotiate with a big bank on a mortgage is incredibly difficult and not often very successful for the average person looking to buy a home. With seller carryback, there’s always room for negotiation.

Potentially Saves Money

Because you can negotiate on just about everything, you might be able to score a lower interest rate, make a lower down payment, and put up no personal collateral in order to make the deal.

However, this is unlikely. Remember, you are a riskier buyer, so you’ll likely need to pay a premium.

Easy Closing

The closing process is far easier with a seller carryback. There’s often less repetition in the process and fewer layers of red tape you have to get through compared to dealing with a lender.

Cons for the Buyer

With a seller carryback, a buyer may experience a few drawbacks, such as:

Negotiation

Yes, negotiation is both a pro and a con. On one hand, you can negotiate terms that are beneficial to you. On the other hand, you have to know what you’re doing in order to effectively negotiate.

Possible Issues With Heirs

If the seller who finances your home dies, then you’ll be a part of the estate and have to deal with their heirs.

You have a contract, so you don’t need to worry too much about this aspect of it. But it could mean a little more personal involvement than what you get with a bank loan.

A Word on Restrictions

When the Dodd-Frank Wall Street Reform Act was passed in 2010, it impacted the way that seller carrybacks work. If you’re a real estate investor who doesn’t plan to live on the property, then you don’t need to worry about it.

But if you plan to occupy the property, then there are a few things you and the seller need to know that can be a bit confusing. Make sure to do your research so you know the ins and outs of the law.

Should You Use Seller Carryback Financing?

Seller carryback financing may be a new concept for you, but it’s not difficult to understand the basics.

We hope our guide helps you decide if it’s the right way for you to purchase your next property or not.

And while you’re here, make sure to check out our other complete guides.