It’s been said that the best way to become a millionaire is to invest in rental property.

After all, it’s a great way to reduce taxes while earning stable cash flow. I’d know—as a former property manager with over 500 units, I’ve learned a great deal about the business.

Introduction to Investment Property

Although real estate is a wonderful investment, it’s often overhyped. The truth is, not everyone should own a rental. In this guide, I’ll explain the reasons why you should buy or avoid rental property.

Before going any further, you should ask yourself a few questions:

- Are you able to completely separate yourself from the things you buy?

- Can you afford to put 2-3 months’ worth of mortgage payments into a separate bank account?

- Would you keep a level head if you drove by your property and saw it in disrepair?

- Are you free of high-interest credit cards or other consumer debt?

If you answered “no” to any of these questions, you should reconsider investing in rental properties. The truth is, it’s not for everyone, and you need to treat your investment like a business.

I’ve managed for many clients who loved the idea of telling their friends and family they own rentals but didn’t have the business sense, annual income, or emotional control to handle big expenses or unexpected tenant vacancies.

If this describes you, don’t despair; you can still passively own real estate through crowdfunding platforms, REITs, mutual funds, ETFs, or even partnerships. We’ll cover those in another post, as this guide is written for owners seeking to learn more about owning physical investment property.

For those wanting to take the next step, ask yourself the following questions:

- Am I seeking to reduce your taxable income?

- Can I capitalize on steadily rising property values?

- Should I use leverage to maximize investment returns?

- How can I earn steady and predictable passive income?

If you answered “yes” to any of the above questions, you came to the right place. In this guide, we’ll explain how to buy, own, and dispose of residential investment property.

Using my experience as a property manager as a base, I’ve sought to make the most comprehensive guide on the internet. While this is a long guide, I’m confident you’ll learn a thing or two about buying rental property. Read on to learn more.

What Is Rental Property?

Rental property is a house or building purchased or built to lease to a third party for a profit. You may hear investment property called many things, but the two main categories include:

- Single Family: A standalone home built for only one family. Often made for owner-occupants and found in neighborhoods or suburbs.

- Multi-family: duplexes, townhomes, and any other building with shared walls that include two or more units.

Rental property is attractive because, as an owner, you’ll earn monthly income and a healthy tax deduction (more on that later) while also benefiting from price appreciation.

Appreciation increases your total net worth as your property becomes more valuable. On average, single-family homes appreciate 3.9% per year, which is typically enough to at least cover inflation.

While multi-family units don’t appreciate as quickly, they typically act like a traditional bond.

This means that, compared to a single-family home, cash flow is more stable, but appreciation is limited. Like a bond, multi-family property is affected by interest rates.

When rates are low, prices increase, and yields (returns) decrease. When rates fall, yields (returns) increase, and prices drop.

Why Invest in Rental Property?

Both types of property allow you to receive steady cash flow that increases each year predictably as tenants renew at higher rates. This cash flow can be used to improve the property, pay a loan, or simply increase the owner’s annual income.

Each owner has a different strategy, which is shaped by everything from their net worth to their risk tolerance. Regardless, the common element is that their properties grant them predictable monthly cash flow.

Tax Benefits

In addition to providing cash flow, rental property also offers the owner significant tax benefits. Many investors even argue that these tax benefits are the main reason they bought their rental property in the first place.

Tax breaks come in two forms:

- Depreciation is the reduction of an asset over time due to cumulative wear and tear.

- 1031 Exchanges: A provision in the IRS tax code that defers tax liability resulting from the sale of a property.

Depreciation

Depreciation

Put simply, depreciation is a phantom expense. Unlike a lawncare or utility bill, there is no outflow of money to a vendor. Instead, it is a reduction in property value from wear and tear.

This is often a difficult concept for novice investors to grasp, so we’ll illustrate this in the best way we know how—by using an example.

Example

Andrew, a property owner, advertises his single-family home for rent. Bob sees an ad and tours the house. He loves it so much that he decided to move in.

During his walkthrough, he notes the home is in tip-top shape with brand new paint, carpet, and kitchen appliances. After Bob moves in, he decides to make the home his own by hanging pictures and other various decorations.

While he was a tidy tenant who respected the property, he scuffed some walls, moved furniture, and wore the carpet down by walking to the kitchen each day.

These things are known as “normal wear and tear.” Simply put, these are things that a reasonable third party would expect from the average tenant.

As a result of normal wear and tear, the property is worth less than it was when Bob moved in. Andrew will need to invest his resources in the property to bring the unit back into like-new condition.

The IRS recognizes this annual reduction in value and allows owners to write off 1/27.5th of the property each year, net of land. If you bought a property for $150,000 and the land value is $10,000, then you can write off 1/27.5th of the remaining $140,000.

In this case, you can deduct $5,090 from your first year’s taxes in the form of a depreciation expense. If your income is less than the depreciation expense, you could even take a loss.

Depending on your ownership structure and tax situation, you could use this to offset business income or roll the loss into the following year.

As you probably guessed, nothing is free, and there is a catch: if you sell the property, you will have to pay taxes on the accumulated depreciation. Fortunately, this can be delayed by using a 1031 exchange.

1031 Exchanges

The second primary tax reason for owning rental property is a 1031 exchange. The largest benefactors of this tax provision fall into two categories:

- Owners in high tax brackets: These owners reap the tax benefits during times they are in upper tax brackets and wait to sell until they are in a lower tax bracket. This strategy is similar to those with non-Roth 401(k)s and other qualified retirement plans.

- Owners with heirs: Heirs to an estate start with a clean slate. This means that their tax basis is “stepped up” to equal the fair market value of the property at the time they inherited it.

Using this tool, a property owner can avoid paying capital gains taxes on the sale of a property if a similar “like-kind” property is identified and purchased within a specific time frame.

Additionally, a 1031 exchange also allows an owner to delay paying depreciation recapture tax. This is a huge benefit because, as we’ll cover later, the tax on a fully-depreciated building can often erase any capital gains at the time of a sale.

Single vs Multi-Family

Before buying a rental property, you must consider your long-term goals and your current financial position. I always suggest starting with houses and moving to apartments, as it’s easier to learn the business with simple homes.

Additionally, single-family homes are less capital-intensive. Fundamentally, both single and multi-family investment share a common goal: buy a property, lease it out, and pocket the difference.

But there are differences between the two types of investments. These include:

Single-Family

- Steady rental demand and price appreciation

- Higher monthly rents

- Fairly liquid (typically sold in 30–60 days)

- Buyers are competing against retail buyers willing to pay more

- More wall and floor space means higher turnover costs

- Each home has a roof and exterior, resulting in higher maintenance costs

Multi-Family

- Occupied units hedge cash flow during vacancies

- Less overall exterior maintenance (1 roof and 1 exterior for many units)

- Higher cap rates than single-family

- Little price appreciation due to multi-family acting like a bond

- Illiquid may take months to sell due to higher prices and limited market

- Many markets are saturated with multi-family product, especially when rates are low

- Higher percentage of neighbor disputes

Ultimately, your decision to buy a multi- or single-family property should be guided by your investment strategy and financial position.

Capital Costs

If most of your liquid funds are being applied to the down payment on your loan, it’d be wise to stick to buying a house.

The reason being that, due to their size, large buildings cost far more to maintain than single-family homes. It’s easier to produce $2,000 for a new air conditioner than it is to replace 20 of them.

Even if the building is newly renovated, bigger properties have higher maintenance costs, and you need to consider whether or not you can cover these costs (along with your overhead) if you were to experience unexpected vacancies.

Maintenance aside, the most important consideration between single and multi-family is capital outlay. More often than not, single-family homes cost far less than an apartment building.

For example, 2020 property prices in Omaha, Nebraska, are:

- 3 bedroom, 2 bath SFH: $175,000

- B-Class multi-family: $75,000 per unit

Keep in mind that these prices are for, on average, a lightly updated property built in the ’80s or ’90s and will require a decent amount of capital improvements.

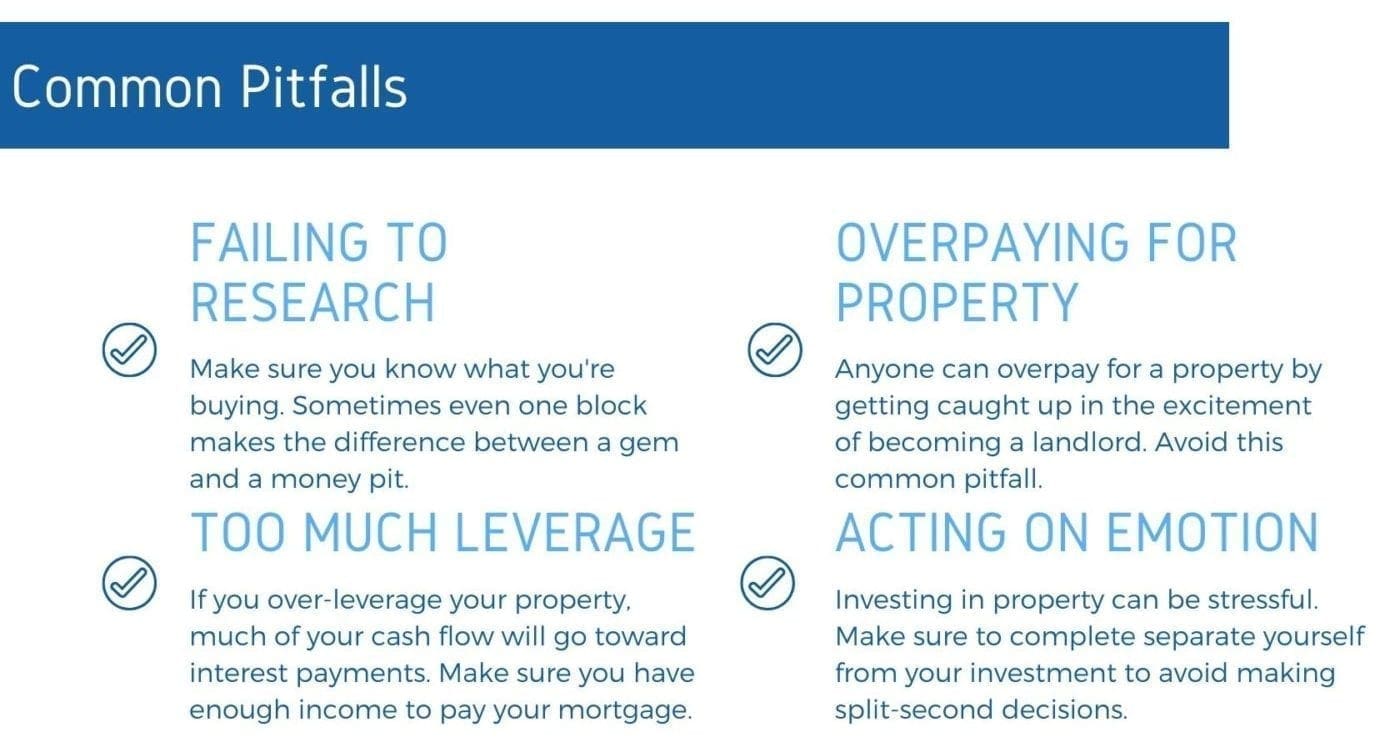

Another thing to consider is that in periods of low interest rates, owners tend to take money off the table. You can certainly still buy a good property in these markets, but don’t buy into the seller’s cash flow claims without doing proper due diligence (more on that later).

Many owners get used to a property’s cash flow and defer routine maintenance, which falls on the new buyer to address.

If you’re buying a well-maintained property, you’ll have to pay for it. Also, most everything on the public listings is property that other investors have passed on.

We’ll cover this later in this guide, but it’s almost always best to buy properties off-market to get the best price. If not, you’re at risk of competing with other buyers or purchasing a run-down property.

If you are eyeing a fixer-upper, you’ll undoubtedly need to set aside money to improve the systems, common areas, or the units themselves. Regardless of which property type you choose, you should remember that cheap is expensive.

In a nutshell, this rule of thumb states that if you buy a low-priced property, you’ll pay for it over time. This could be through expensive repair bills, capital improvements, high vacancy costs, or tenant damage.

I can’t even begin to describe the number of times clients brought me a property to manage, thinking they’d get a great monthly return because they paid little for it.

Unfortunately, they quickly learned that the price was low for a reason and ended up costing some of them their entire portfolio. For this reason, I always recommend making the necessary investments upfront or over time.

If you are eyeing a multi-family property that needs some work but don’t have any money to invest in capital improvements, it may be worth considering one or more well-maintained single-family homes.

Markets

Another factor to consider is that markets are very cyclical, which affects the total number of units in the market and demand for those units. When interest rates are low, developers build apartments.

After all, cash flow is predictable when rented, and bigger properties can be sold to insurance companies and pension funds. As a result, this affects property values and overall market rents.

While each market varies based on total supply and demand, too much supply can severely reduce your cash flow, so it’s something to consider. Big brokerages like CBRE make it easy to spot trends by highlighting both regional and national markets in various reports released throughout the year

You may even find that A-class apartments are overbuilt, but B-class properties are lacking, which would potentially make a B-class property worth considering.

Or maybe you’ve found that 1031 buyers are hungry for newly renovated properties, which would present an opportunity to buy a run-down building to renovate and sell.

In any situation, your investment strategy will guide your decisions, and being flexible and knowing your market will make it easy to spot investment opportunities.

Retail Buyers

While single-family home prices fluctuate, they tend to appreciate due to steady demand from retail buyers continually.

The Great Recession of 2008 caused many homebuilders to shut their doors. And many of those who weathered the storm began focusing on high-end homes with more significant margins.

Zephyr_p/Shutterstock

The result is a reduction in new starter homes being built, which puts upward pressure on existing home prices as new buyers enter the market.

For owners of investment homes, this is beneficial because it increases their equity. Healthy demand also makes the home easy to sell if the need arises.

However, it also makes it more expensive to find a home that makes sense to use as an investment property.

But don’t get discouraged just yet, because there are a few creative ways to avoid paying a premium by buying off-market properties. And you can bet we’ll discuss them later on in this guide.

Other Considerations

In addition to the market and capital costs, there are some less-important factors to consider before determining what type of property to buy. For example, a multi-family property houses multiple units inside 4 exterior walls.

This means that on a per-unit basis, your exterior maintenance costs will be less than a home. Also, you’re able to hedge your cash flow when a tenant gives notice because your other tenants are still paying rent.

If a hail storm hits your area, you’ll only file one claim for the roof and siding. Finally, because multi-family property houses all units in one central location, it’s much easier to visit all groups at once.

With a portfolio of homes, you’d have to drive across town to walk them. This makes management much easier and helps you keep a close eye on what your tenants are doing.

This is an important consideration and is the reason many investors sell individual homes to buy a single property.

Another overlooked consideration is average turnover time and vacancy cost. While your market will vary, I’ve found that the average multi-family tenancy ranges from 12 to 18 months, while my single-family occupants typically stay between 18 and 24 months.

However, this is offset by my average turnover cost. Because there is typically less square footage in an apartment, my average multi-family turnover costs $1,000. Conversely, the average single-family turn costs $1,800.

I’ve found that average unit vacancy varies depending on the time of year, location, and class of property. But if the home is buttoned up and is reasonably priced, both multi and single-family rentals average the same vacancy time of 30 days between tenants, which equates to 7% annually.

Finally, single-family homes have higher appreciation averages. Still, unless you have multiple units, your income is eliminated during a vacancy.

Because of this, I recommend that investors seeking appreciation buy single-family homes and investors seeking cash flow buy multi-family buildings.

Investment Property Returns

Stoatphoto/Shutterstock

Average returns vary largely by economic cycle, location, upkeep, and property class. Additionally, single and multi-family homes measure returns in different ways. Single-family home investors typically use cash-on-cash returns, and multi-family investors use cap rates.

Single-Family

Many financial experts will advise a return exceeding 8% is good. After all, the S&P 500 has averaged returns of just under 8% since 1957. Measuring single-family home returns is slightly more complicated, as you’re dealing with debt and tax breaks.

Overall, single-family home investors should expect returns between 5% and 20%. While this might seem like an unusual range in returns, the amount of debt affects the total return. Generally speaking, a little debt will increase the return an investor gets on his initial investment.

This is known as a “cash-on-cash” return and is best explained in an example. Because this is only meant to highlight the effects of leverage, we’ll exclude any tax benefits received.

Investor 1

- Purchase price: $100,000

- Initial investment: $100,000

- Annual rent: $12,000

- Operating expenses: $5,000

- Total return: 6%

To calculate this return, we’ll take our annual rent ($12,000), subtract our operating expenses ($5,000), and divide the result by the initial investment ($100,000). While this investor will make money on his investment property, his return is only 6%.

Investor 2

- Purchase price: $100,000

- Initial investment: $20,000

- Annual rent: $12,000

- Operating expenses: $5,000

- Interest expense (6%, 30 year am): $4,800

- Total return: 11%

Because Investor 2 used leverage, his returns are much higher. We’ll use the same formula as we did before, but this time we’ll add the interest expense to our operating expenses. As you can see, the total dollar return is smaller, but so was the initial investment.

We’ll get into rules of thumb in the next section, but I like to use the 50% rule, which states that half of the total gross rent will be spent on operating expenses. These expenses include property taxes, recurring maintenance, property insurance, vacancy, and rent concessions. This does not include debt service.

Many investors will find that, after paying operating expenses, they don’t have enough money left to pay their mortgage. I’ve seen many would-be investors fall into this trap.

The truth is, single-family homes are typically not meant to generate high amounts of cash flow, so you likely won’t be taking any distributions.

At best, you’ll break even after paying your mortgage. Over time, through a combination of rent increases and principal reduction, the spread between the gross rental amount and your debt service will increase.

Smart investors invest this money back into the property, making it more attractive. This ultimately reduces vacancy and increases market rent. At the end of the day, you’re left with a property that mostly paid itself off.

Additionally, you benefit from capital appreciation. Assuming property continues appreciating 3% annually, the $100,000 property from our example will be worth roughly $242,000 after 30 years.

This means Investor 2 would have made a 12x return on his money, which shows the power of combining leverage with compounding interest. This example is an excellent illustration of why we recommend buying single-family homes for appreciation and multi-family property for cash flow.

Multi-Family

While single-family performance is measured using use the cash-on-cash returns, multi-family performance is measured using a cap rate. Put simply, this measures the total return, net of operating expenses, as a percentage of the property’s market price.

Generally speaking, multi-family properties don’t appreciate as quickly as single-family homes, mainly because there is less demand for expensive buildings than there is for single-family homes. As a result, these investments trade like bonds.

When interest rates increase, prices fall. Because investors primarily finance their multi-family purchases, this means that it’ll cost more to service debt on their investment. Naturally, this leads to falling prices, which increases cap rates.

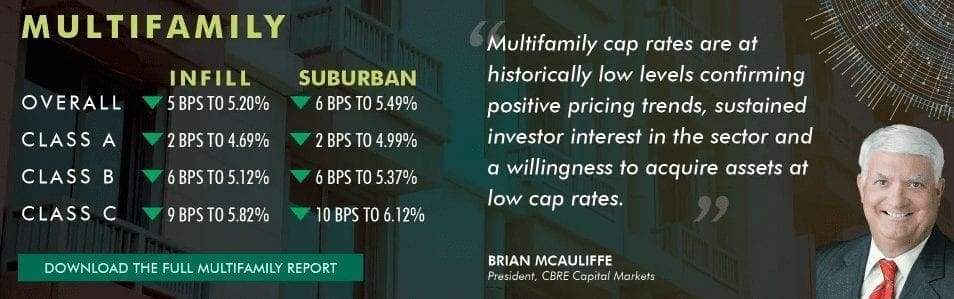

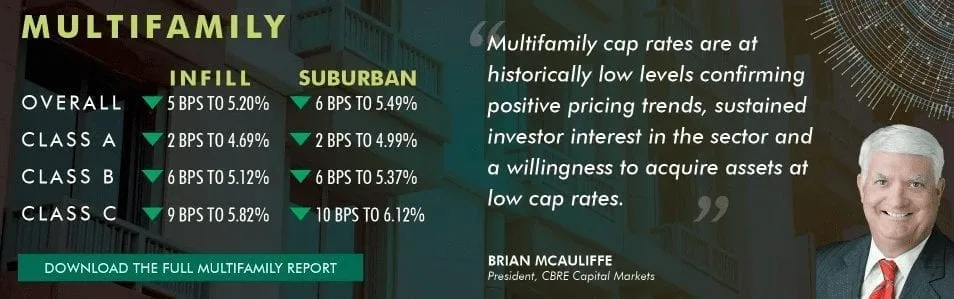

In 2020, interest rates are historically low, which has increased prices, thereby reducing cap rates. One of my favorite resources is CBRE’s annual North American Cap Rate report. This report highlights the national cap rates, broken down by category.

Source: 2019 CBRE Cap Rate Survey

As of 2019, this report listed the Infill and Suburban (respectively) rates as follows:

- Overall – 5.2, 5.49

- A Class – 4.69, 4.99

- B Class – 5.12, 5.37

- C Class – 5.82, 6.12

With interest rates between 6% and 7%, these returns don’t look very good. Say you bought a C Class property in the suburbs and financed it at a 7% interest rate. Based on these cap rates, you’d lose 88 basis points per year on your investment.

That said, these numbers are averages, and it’s still possible to find off-market deals at lower prices, which results in a higher cap rate. In my portfolio, I’ve seen multi-family cap rates average 7%-9% in the last few years.

However, it’s worth noting that there’s been a lot of money moving out of California and Colorado and into more conservative states through 1031 exchanges. As we stated earlier, investors have 45 days to identify a property to defer taxes on a sale.

If you remove the 1031 exchanges from this average (those buyers are overpaying for new properties to defer taxes on the gains), I will venture to guess that cap rates would average 6%-7%.

As I said before, I recommend that investors seeking appreciation buy single-family homes and investors seeking cash flow buy multi-family buildings.

Real Estate Investing Rules of Thumb

Now that we’ve highlighted the differences between properties, you should know some basic rules of thumb to help guide your investment decisions. Of course, these are just that – rules of thumb. So they don’t apply to every investor.

However, I manage 500 units and have tested these rules many times. More often than not, they’re relatively accurate, +-10%. If anything, these rules help you use “napkin math” to determine an opportunity’s expected return quickly.

- Rule of 72 – Dividing 72 by a fixed annual rate of return determines how quickly you will recoup your investment.

- 1% Rule – If you can rent your property for 1% of the purchase price, you should be able to make your mortgage prices using rent proceeds.

- 2% Rule – More conservatively, if your monthly rent exceeds 2% of the purchase price, you should be cash flow positive (after factoring in operating expenses)

- 50% Rule – On average, half of a single-family home’s gross rental income will be spent on operating expenses like taxes, insurance, vacancy, turnover, and upkeep costs.

As you can see, rental property offers many benefits, the most valuable of which is the ability to use leverage to increase returns significantly. However, success in real estate all comes down to buying the property for a reasonable price. If you overpay, you’re sure to fail.

I’ll say that again: DO NOT OVERPAY FOR YOUR PROPERTY.

Fortunately for you, we’ve created a complete guide to buying an investment property. In it, we outline the best ways to source off-market properties, so you don’t overpay.

Click the button below to see our favorite ways to buy rental property from motivated buyers. We’re sure you’ll thank us later.