A secondary market is where buyers and sellers can trade in financial and other sorts of products that were initially created by someone else.

The home resale market, the stock market, and the market for mortgage-backed securities are all types of secondary markets.

What Is the Secondary Market?

The primary market is where something is sold for the first time. For instance, a company holding an initial public offering (IPO) of shares sells the new issue on the primary capital market.

After the IPO on the primary market, new stocks trade in the secondary market. The secondary stock market includes exchanges such as the New York Stock Exchange, NASDAQ, and the over-the-counter market.

Bonds, mutual funds, and other financial assets also trade on these secondary markets. In real estate, sales on the primary market happen when a homebuilder sells a home to a homebuyer.

After the initial sale, if the home is sold again, it happens on the secondary market. Secondary markets are crucial for many industries.

The volume of business in secondary markets is often a great deal higher than it is in primary markets.

An automobile, for instance, may be sold several times to different owners after the first buyer drives it off the lot. Secondary markets also exist for books, event tickets, furniture, and many other products.

Real Estate Secondary Markets

In real estate, a large majority of home sales are resales that occur in the secondary market. The National Board of Realtors said existing home sales in July 2019 happened at a rate of 5.42 million per year.

The Census Bureau recorded 685,000 transactions for new home sales in the same month. About eight times as many home sales occurred in the secondary market in that month.

Without the secondary market for homes, few real estate professionals could make a living in the business. After all, that’s where the bulk of their business lies.

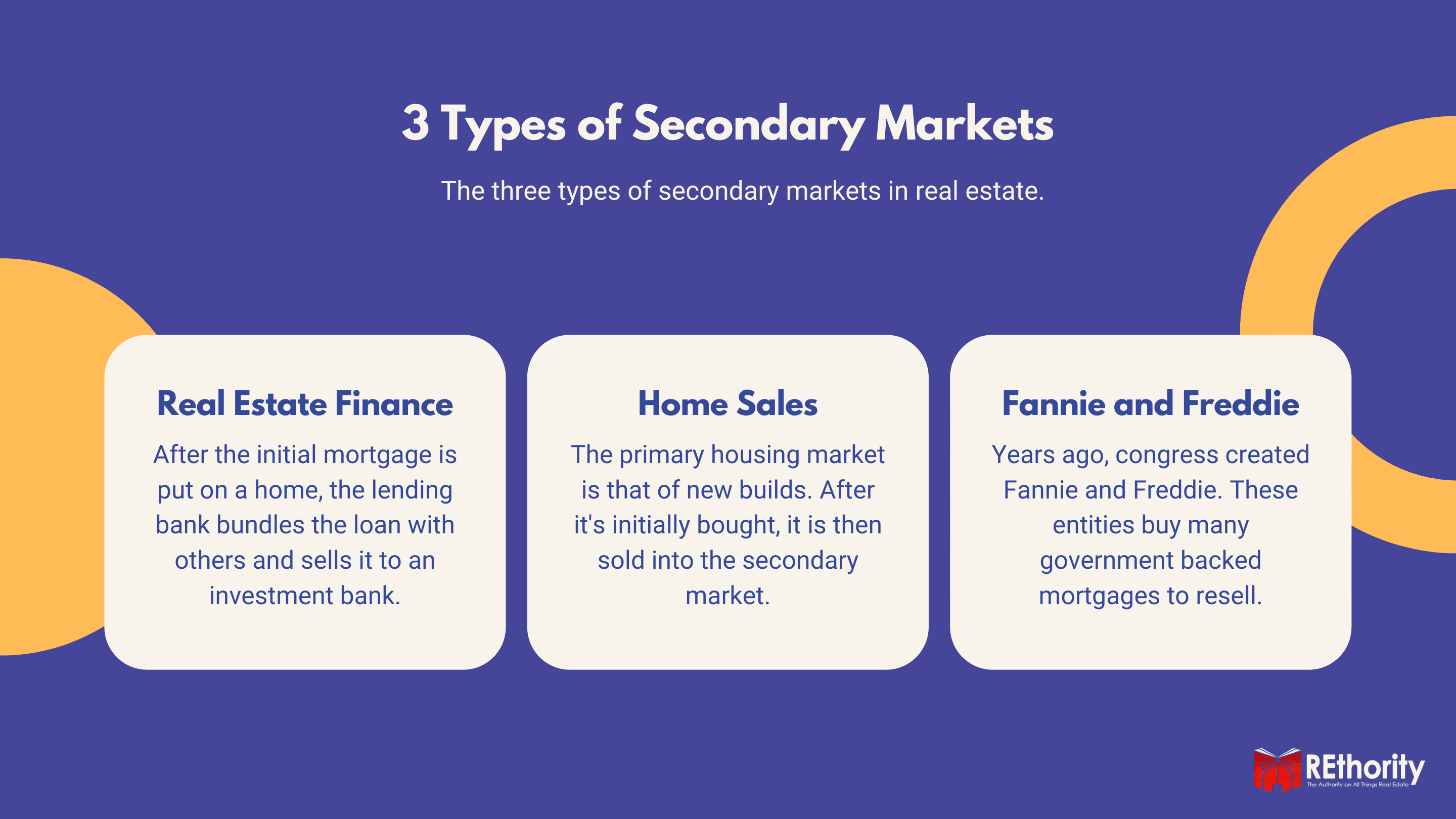

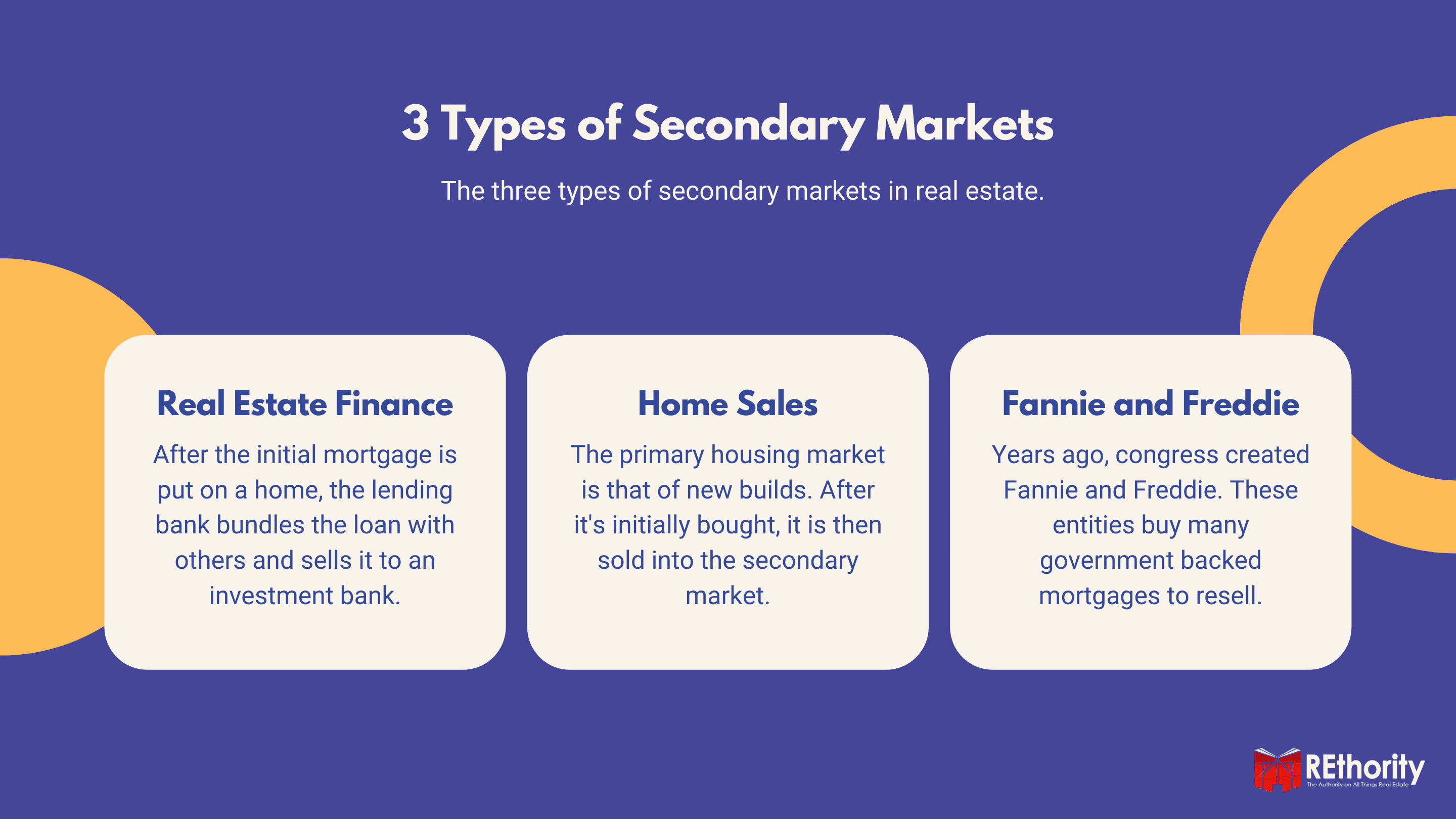

Secondary Markets for Real Estate Finance

Secondary markets are also important for financing real estate purchases. When a buyer purchases a home, the mortgage lender creates a loan. This loan origination is the primary market transaction.

After that, many mortgages are bundled together and sold on the secondary market as securities. After securitization, the loans are known as mortgage-backed securities (MBSes).

Investors buy MBSes to receive the income as the borrowers pay the loans. Without the markets for trading securities backed by mortgages, buyers would find it more difficult to get financing.

If mortgage originators didn’t sell loans on the secondary market, they would soon run out of money to lend. Packaging and selling mortgages on the secondary market allows mortgage lenders to replenish their vaults.

Then they can make new loans. In this system, the originators make money on the deals by charging origination fees. The MBS buyers make money off the interest they receive.

How the MBS Market Works

When a homebuyer takes out a mortgage, it is combined with other mortgages that have similar financial terms. For instance, 30-year mortgages with a fixed 4 percent interest rate will be pooled together.

Another pool might be made of 15-year mortgages with a 3.5 percent rate. Pools could have adjustable-rate mortgages, jumbo mortgages, and other kinds of mortgages.

From these pools, similar mortgages are bundled together and sold as mortgage-backed securities. The mortgages in the bundle back up the value of the MBSes.

There wasn’t always a market for MBSes. Only big financial institutions could lend money for 30 years. The lack of mortgage competition made it harder and more costly for homebuyers and investors to get loans.

Fannie and Freddie

To address the liquidity problem, Congress created the Federal National Mortgage Association (Fannie Mae) and the Federal Mortgage Corporation (Freddie Mac).

These shareholder-owned companies buy most of the mortgages created in the U.S. and sell them to investors.

The resulting secondary market for mortgages makes mortgages easier to get than before. The resulting demand keeps rates competitive, thereby making loans easier to obtain.

Investors who buy MBSes have a great influence on the mortgages homebuyers and investors get. The paperwork at a real estate closing, for instance, helps satisfy investors that a loan will not be too risky.

MBS requirements for things like title insurance, appraisals, and inspections are responsible for many of the fees paid at closings. Monthly mortgage insurance premiums are necessary to make low-down-payment loans attractive to MBS investors.

Before the 2008 housing slump, MBS investors used faulty financial models to estimate future market movements. As a result, overly risky subprime loans were issued, and home prices skyrocketed.

When the risky nature of the subprime loans was revealed and home prices began to falter, some large real estate lenders went bankrupt. Wall Street firms that had gotten rich off MBSes also went under.

Today, the standards for underwriting mortgage loans are much stricter than in the early 2000s. Much of this is due to MBS investor concern about avoiding a repeat of the last catastrophe.

The Mortgage Servicing Market

Two sorts of transactions happen on the secondary mortgage markets. One happens when the originator sells the loan. The other type is when the originator transfers the servicing of the loan.

The buyer (or buyers of the MBS) are entitled to interest on the payments. The new loan servicer simply acts as an agent for receiving the payments.

Loan servicers are often big banks, such as Wells Fargo, or financial service institutions that specialize in performing this task.

These firms are paid to receive the payments and pay principal and interest on the loans.

If the mortgage payment includes amounts for hazard insurance and property taxes, the servicer collects those as well. Then the servicer is responsible for seeing that insurance and taxes get paid.

The loan servicing market is very important. Companies specializing in loan servicing do it cheaper and better than companies focused on originating loans. So borrowers save money and get better service.

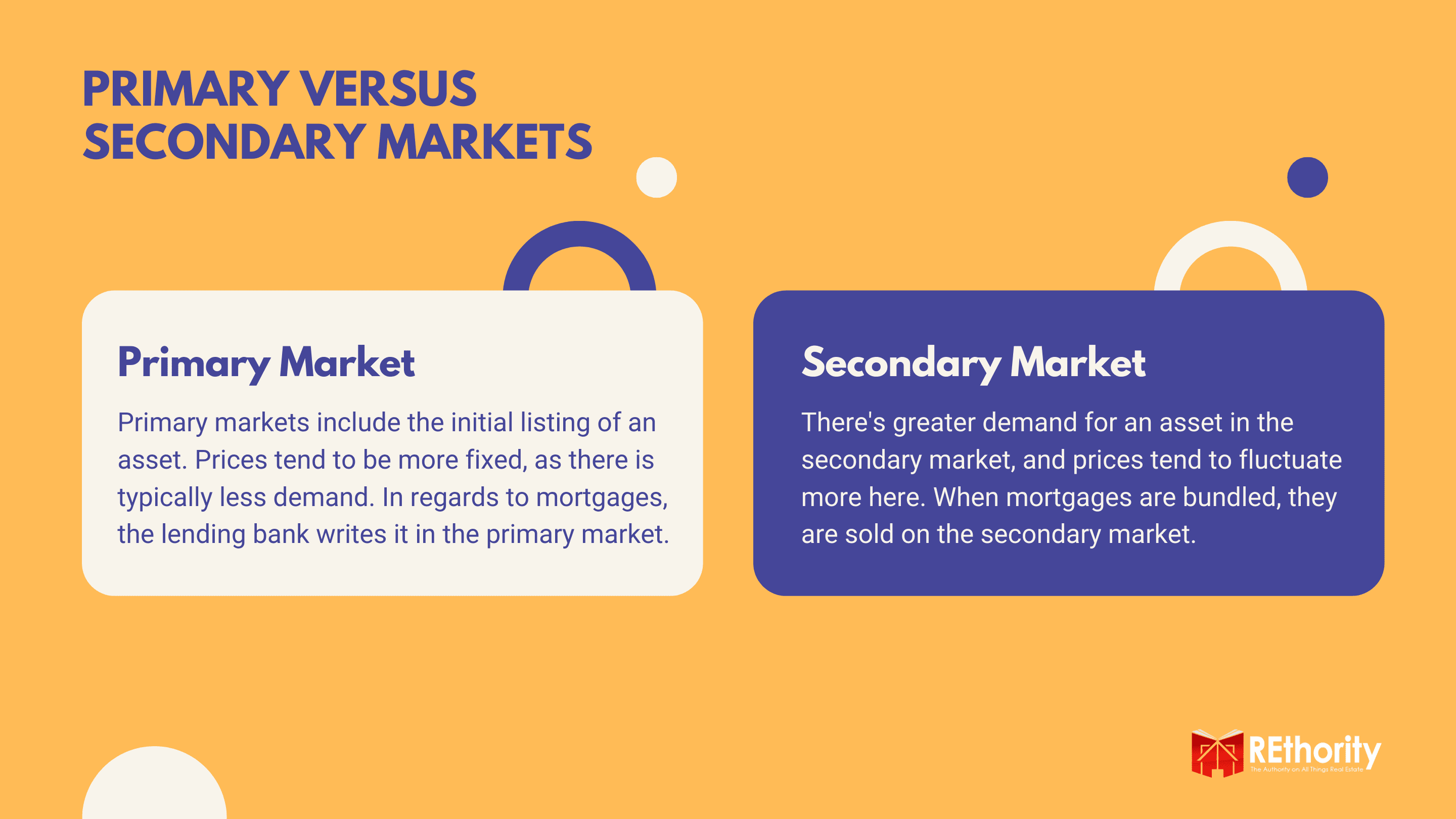

Primary vs Secondary Market

One of the big differences between primary and secondary markets is that prices are typically more fixed in primary markets.

Companies doing IPOs set the target price for their shares. On the secondary market, supply and demand determine pricing.

Sometimes the actual price of shares in an IPO varies from the issuing company’s target price. But it’s generally close.

On the secondary market, prices can quickly change as a result of investor sentiment, market trends, and news events.

The same happens in housing. Builders choose the price at which their new homes will sell. They can’t do this independently of the market, of course. New home prices have to bear some relationship to supply and demand for new housing.

However, new home prices have an impact on resale prices. Generally, resale homes will be priced about 25 percent less than similar new homes.

There is also much less action on primary markets. It’s easier for buyers to find homes, MBSes, and stocks to buy on secondary markets than on primary markets.

Secondary markets are essential because they let sellers find buyers. Without secondary markets, a homeowner buying a house would have to own it forever. Investors would never be able to cash out.

Summing Up the Secondary Market

Homebuyers and investors buy and sell their properties on secondary markets.

Mortgage loans and the job of servicing loans are also traded on secondary markets.

However, there is nothing second-rate about the importance of secondary markets in real estate.