An automated valuation model (AVM) runs real estate data through computer algorithms to generate values for real estate properties.

This means appraisals can happen faster. Read on to learn more.

What Is an AVM in Real Estate?

AVMs offer alternatives to traditional appraisals by professional appraisers and are increasingly accepted by the real estate industry.

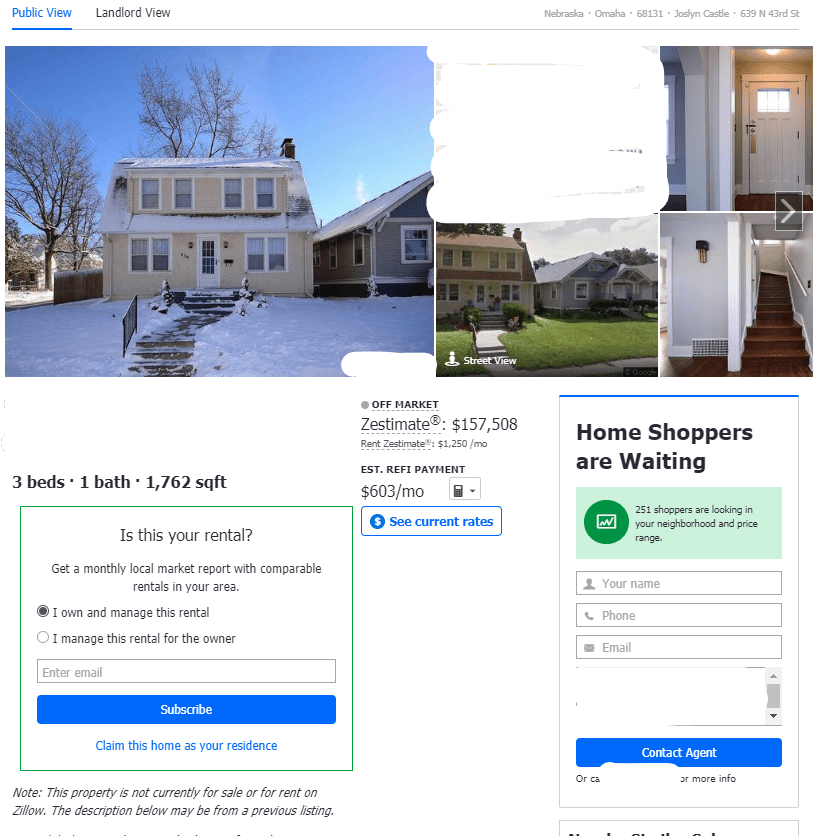

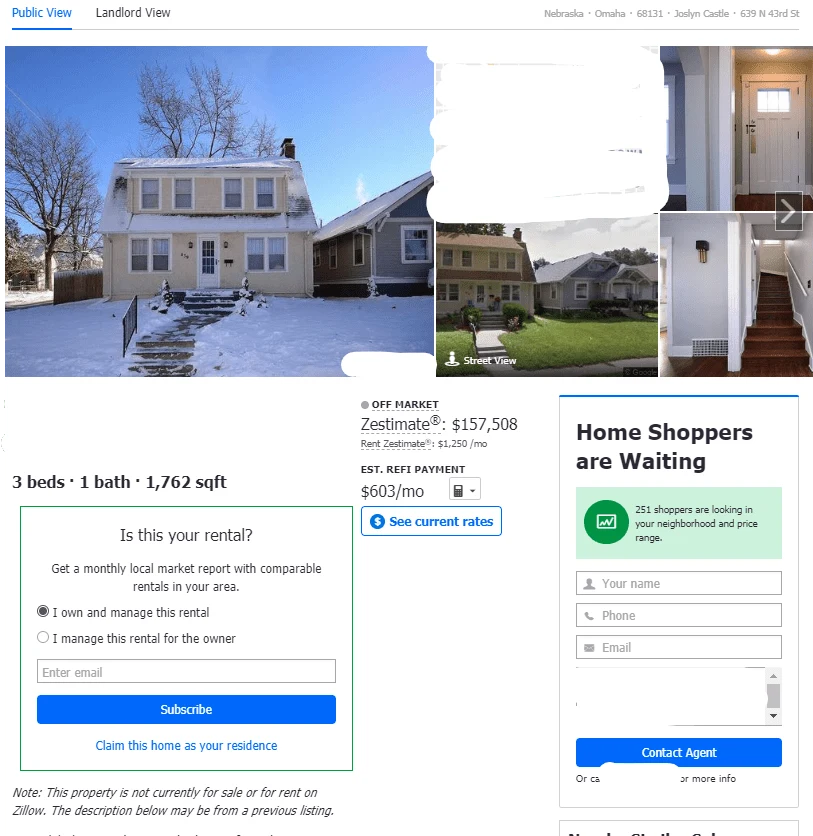

The best-known AVM is probably Zillow’s Zestimate. This is one of the first public AVMs and has been used by millions of homeowners and homebuyers to estimate the market value of residential real estate.

There are a large number of other AVMs as well. Some are offered by real estate organizations to provide value estimates to professionals.

The National Association of Realtors has its RVM for real estate agents and brokers, for instance. And real estate information provider CoreLogic supplies AVM services to mortgage lenders.

Read on to learn how AVMs are changing the real estate game by either helping appraisers be more efficient or by cutting them out altogether.

How an AVM Works

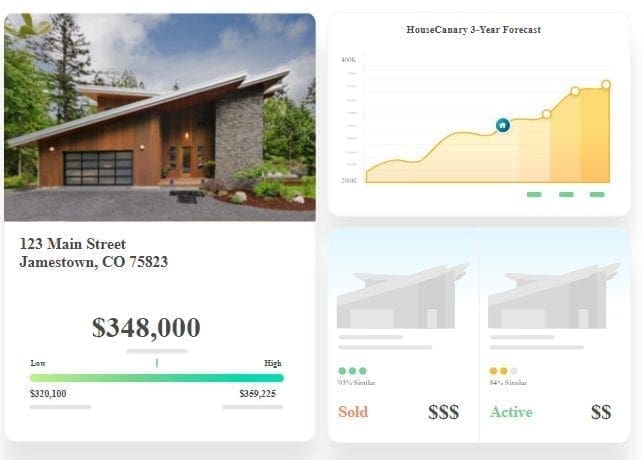

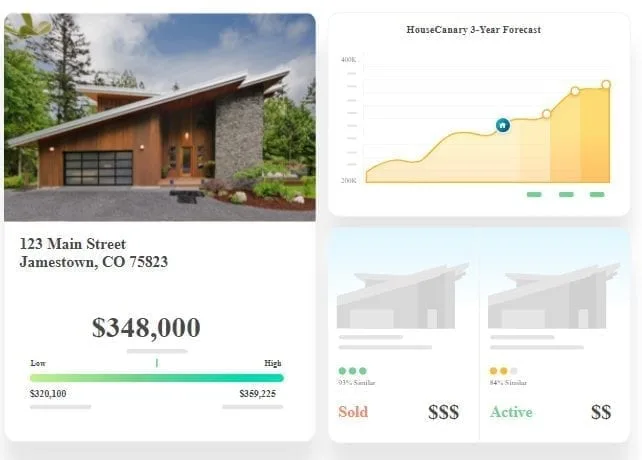

AVMs start by tapping the digital information on the real estate market that is available today. When that data is run through computer algorithms, AVMs can generate estimated property valuations.

Image Source: Housecanary.com

The market data used to calculate property value can include the following:

- Past sales history

- Square footage

- Past listing prices

- Number of bedrooms

- Number of bathrooms

- Other property features, such as pools

- Tax appraisal value

- Taxes paid

- Comparable sales

- Price trends

The algorithms are mathematical formulas developed by economists, statisticians, and data scientists. These formulas statistically analyze the data on a property as well as similar properties to produce a written estimate of the value of that property.

Every AVM has a unique formula that incorporates different variables and assigns different weights to them to calculate home prices. AVMs also tap various sources of data. So different AVMs produce different values for the same property.

New data is continually being updated, as often as daily. The algorithms are also updated to reflect changes in market trends.

Importance of Accurate Valuations

Rawpixel.com/Shutterstock

Accurate valuations of real estate property are essential to all parties to a transaction. Buyers don’t want to overpay. Sellers don’t want to leave money on the table.

Vacant Property

Real estate agents want to be able to give their clients accurate advice on the likely selling price.

A higher price produces a higher commission since agents are usually paid a percentage. But too high a price may cause a property to sit for a long time on the market.

Accurate Loans

Perhaps most importantly, lenders don’t want to lend more money than a property is worth. Since lenders control the funds to purchase most real estate, lender requirements drive the need for accurate valuations.

As a result, most real estate transactions require valuations of some kind. Human appraisers perform the majority of appraisals. These are professionals trained and licensed to provide accurate and objective appraisals. They are paid a flat fee for the appraisal.

Objective Appraisals

Appraisers are unlike everyone else involved in a transaction, including buyers, sellers, agents, and lenders. That’s because they don’t have a direct interest in the appraised value.

They get paid, whether it’s more or less than what is expected or desired. Sellers, of course, want a higher valuation. Buyers wish for a lower valuation. Lenders just don’t want the appraisal to be more than the actual value.

How AVMs Are Used

Homeowners often use AVMs like Zillow’s Zestimate to get an idea of what their properties might sell for. Buyers use these public AVMs to find out what they might expect to pay for a home.

Real estate agents use AVMs like the NAR’s RVM to get an idea of a property’s value. This is crucial to setting a listing price.

However, the NAR warns that an RVM, which uses listing prices from the local Multiple Listing Service, is not the same as a competitive market analysis (CMA). A real estate agent uses the sales of comparable homes to prepare a CMA.

Image Source: Zillow.com

A broker’s property opinion (BPO) is another sort of valuation that is often used with foreclosure homes. It may consist of little more than driving by the property to make sure it is there.

Lenders also use AVMs to try to avoid lending more than a property is worth. This is why any home that is purchased using a mortgage typically has to have an appraisal; few lenders accept AVMs.

iBuyers, on the other hand, typically use only AVMs to determine the value of a home. Offerpad uses an AVM to set the amount of an all-cash offer it will make for a home. These iBuyers may not use appraisals at all.

Even such industry goliaths as the Federal National Mortgage Association (Fannie Mae) are using AVMs. Fannie Mae’s Home Value Explorer is used for underwriting mortgages, managing risk, and even purchasing qualified homes, all without appraisals.

Advantages and Limitations

Compared to human appraisals, AVMs offer some appealing advantages, but they also present some challenges Read on to learn why.

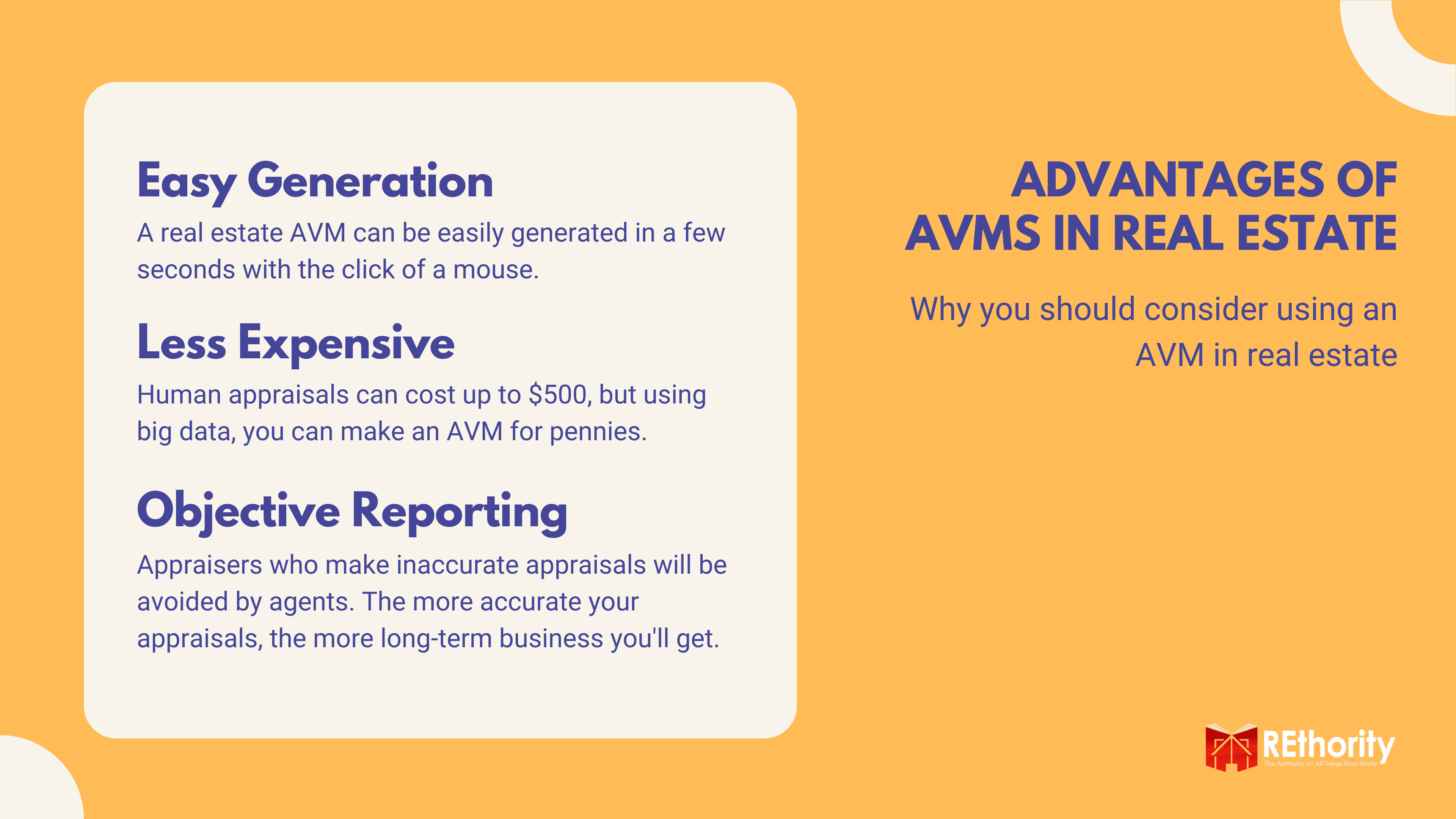

Easy Generation

First of all, they are fast. It can take two weeks to schedule a visit from a human appraiser and get the results. By comparison, an AVM can generate a valuation in seconds.

Less Expensive

AVMs are also less expensive. While a professional appraisal of a single-family home can cost $500, an AVM from Zillow is free.

Also, AVMs are genuinely objective. They aren’t subject to pressure of any kind from buyers, sellers, agents, or lenders.

Objective Reporting

While appraisers are not directly interested, they often know in advance what value the lender needs to make the loan.

And appraisers who consistently produce low values may be avoided by real estate professionals who are mostly interested in doing the deal.

Readily Available

AVMs are also readily available online. A homeowner can get an AVM by simply typing his or her address into an AVM using a smartphone.

AVM Limitations

As you have likely figured out, an AVM does have its downsides. Don’t worry; we’ll recap them for you.

Omits Property Condition

The major limitation of AVMs is that they don’t consider the condition of the property.

An AVM doesn’t know if the paint is peeling or if the basement floods. Many other issues that could significantly affect the property’s value will not be evaluated by an AVM.

Data Can Be Skewed

Also, AVMs are only as good as the quality of their data. Sales prices and other public records of transaction data acquired from county recorders’ offices are often months out of date. That can lead to an inaccurate valuation.

Needs Recent Sales

AVMs also don’t work well when there are few recent comparable sales. However, the same limitation applies to appraisals. Another limitation is that most mortgage lenders require appraisals.

They won’t accept an AVM in place of a report from a trained, licensed professional appraiser who physically inspects the property.

Not Always Accurate

Finally, there are questions about AVMs’ accuracy. Comparing values for the same property by different AVMs will generally produce a range of figures. AVM valuations may vary by 5 percent up or down.

On a $200,000 home, for instance, this could mean valuations ranging from $190,000 to $210,000, a net difference of $20,000. However, human appraisals may not be any more accurate.

The Department of Housing and Urban Development did a study that found 9 percent of appraisals for reverse mortgages were inflated by 20 percent or more.

Using Your Report

One way to use AVMs effectively is to get valuations from several different AVMs. This way, the differences in the way the AVMs calculate will average out and increase the chances of an accurate valuation.

AVMs that may be used to generate valuations include:

The Future of AVMs in Real Estate

AVMs have been used by organizations like Fannie Mae for decades to help manage risk and assign value to real estate. Their advantages of cost and speed seem likely to make them increasingly common in real estate.

As AVM providers refine their algorithms and get access to more and more current data, accuracy will likely increase, and they’ll be used for more purposes.

For now, however, most mortgage lenders still require appraisals, so human appraisers aren’t going to go away for the foreseeable future.

For real estate professionals as well as homeowners and buyers, AVMs provide added insight into the crucial question of what a given property is worth.

While AVMs aren’t perfect and don’t give the final answer, they are valuable tools for any real estate professional, buyer, or seller.